Table Of Contents

Abstract

Companies are under growing pressure to commit to net-zero emissions, and this has pushed Environmental, Social, and Governance (ESG) metrics into the spotlight of climate risk reporting. However, major ethical concerns remain—especially around transparency gaps and the risk of greenwashing. This study systematically reviews literature using the PRISMA framework to examine ethical challenges associated with ESG-based climate disclosures and corporate net-zero commitments. The review points to three main issues: the reliability of carbon disclosures, whether ESG metrics align with global climate goals, such as the Paris Agreement, and the accountability of companies when they claim net-zero targets. The findings reveal widespread inconsistencies across Scope 1 to 3 emissions, with many firms relying on offsets that cannot be adequately verified, while assurance processes remain generally weak. The study contributes by clarifying ethical gaps in ESG reporting and highlighting the need for sector-specific standards, stronger governance structures, and regulatory measures to ensure the credibility and effectiveness of climate action.

Introduction

The integration of Environmental, Social, and Governance (ESG) metrics into corporate climate risk reporting has become a defining feature of current sustainability strategies. As investors, governments, and society intensify demands for net-zero commitments, ESG disclosures are increasingly used to assess corporate climate performance and risk exposure. The need for companies to achieve zero carbon emissions has made ESG reporting a fundamental element of their business plans.

The use of ESG metrics for evaluation has led to various ethical problems that now affect transparency and consistency.Even after concerns regarding inaccuracies in emissions reporting and the risk of false carbon offsets, which foster mistrust in companies’ claims, ethics remains a significant concern. It lies at the centre of the issue.

Arvidsson & Dumay (2021) indicated that improved ESG reporting does not necessarily translate into improved environmental outcomes. A company might exploit its high ESG rating to clean up its image without actually changing its climate direction.Moreover, ESG metrics are not always aligned with global standards, such as the Paris Agreement. In practice, companies primarily focus on financial results over the next few quarters while ignoring sustainability goals in the far future (Hoang, 2023).

Among the issues currently faced, the need for more trustworthy and comparable ESG data to inform stakeholders’ moral choices is a key concern. Stakeholders also use such data to verify corporate promises and assess whether these commitments are being fulfilled through concrete action.

This article thoroughly investigates the issues by delving deeply into them.To achieve this, it collects high-level studies on Scopus to explore the questions related to the morality of carbon disclosure, the compatibility of ESG measurements with climate policy objectives, and the trustworthiness of corporate net-zero commitments. Among other issues, the concerns raised centre on the accuracy of Scope 1–3 reporting, the risks of double-counting, the use of untrustworthy carbon offsets, and difficulties in linking ESG measures to international frameworks such as the Paris Agreement and the IPCC guidelines. The literature discloses climate-related goal gaps and action inconsistencies in corporations with the problem of greenwashing, unstable reporting standards, and the call for effective assurance systems, which will promote transparency and stakeholder trust (Vaio et al., 2025; Sneideriene & Legenzova, 2025; Christy et al., 2023; Ma et al., 2023; Sharaf-Addin, 2024; Hettler & Graf--Vlachy, 2023; Velte et al., 2020; Widyawati, 2019).Furthermore, this review aims to analyse current ethical behaviour in depth and suggest several ways for ESG to become more reliable and effective in mitigating the climate crisis.

The study is structured as follows: Section 2 outlines the objectives; Section 3 explains the research methodology; Section 4 shows the literature review; Section 5 discusses the findings; Section 6 highlights theoretical contributions; and Section 7 presents the conclusion.

Objectives of the Study

This study aims to consolidate earlier results by reconciling different theoretical perspectives and ideas via an extensive review. The objectives of the study are:

To examine ethical issues in ESG-based climate disclosures, with particular attention to transparency, comparability, and greenwashing risks.

To assess the extent to which corporate ESG reporting aligns with global and national climate policy frameworks.

To evaluate corporate accountability mechanisms related to net-zero commitments and climate risk reporting.

Methods

The studies that focus examined ESG metrics, carbon disclosure, and net-zero targets, with an emphasis on ethics and policy alignment. The process employed the PRISMA method to ensure completeness and transparency.

Database Selections and Search Terms

The study examined ESG metrics, carbon disclosure, and net-zero targets, with a primary focus on the ethical aspects and policy alignment. It also covered systematic reviews, bibliometric research, and empirical studies as the main types of academic literature. In this study, a systematic literature review predominantly used three databases: Web of Science, Scopus, and Google Scholar databases, which were selected as the premier sources for global academic literature (Aghaei Chadegani et al., 2013). The following keywords were employed to search the selected databases:

-

“ESG Metrics” and “Climate Policy”

-

“ESG Metrics” and “Corporate Commitments”

-

“ESG Metrics” and “Ethical Challenges and Best Practices for Carbon Disclosure”

Criteria for Selection of Publications

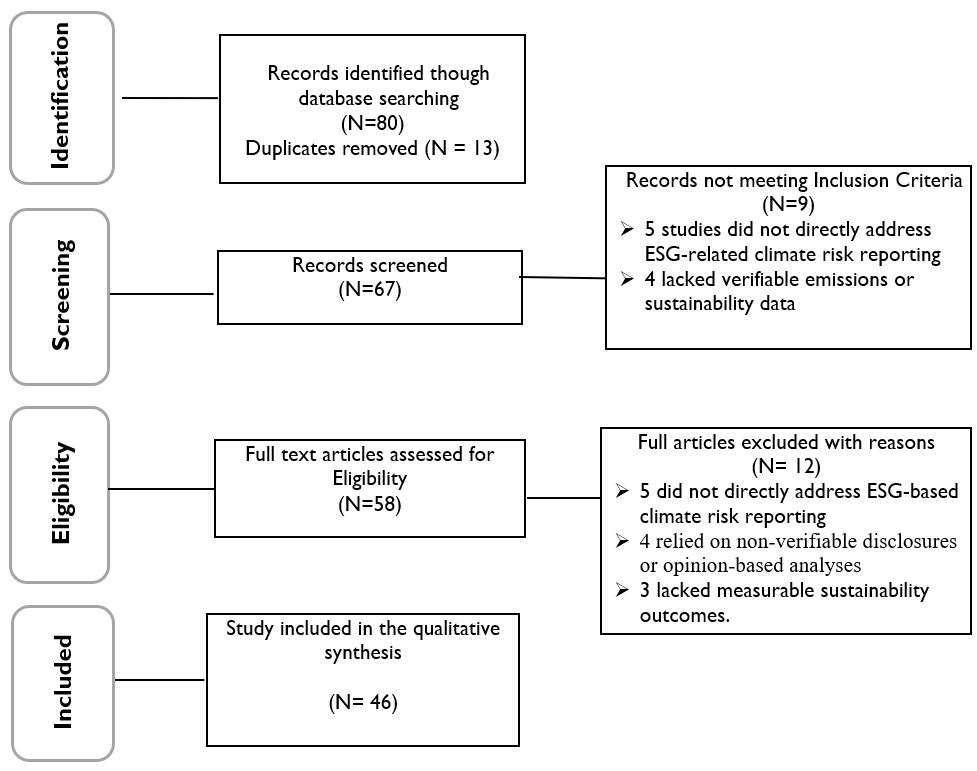

The papers in the consideration list were supposed to be either peer-reviewed articles or conference papers. As such, journals, reports, and books were excluded from consideration. The publication should have been done between 2014 and 2024. In the first stage, 80 papers met these conditions; however, during screening, 34 papers were excluded due to lack of relevance, duplication, or insufficient focus on ethics or climate alignment, so the study was based on 46 papers.

Systematic Literature Review

A systematic literature review (SLR) is a methodical approach to gathering and evaluating contemporary knowledge in a specific field of study. It involves the systematic collection, summarisation, interpretation, explanation, and integration of relevant literature to gain a comprehensive understanding of the subject matter (Okoli & Schabram, 2010). The multidisciplinary study approach is diverse and well-established. It has been adapted to incorporate the plan, performance, and report procedure within our specific environment (Sony & Naik, 2020). Figure illustrates the systematic procedure, which yielded 46 publications for the systematic review.

Source : Developed by the Author

Literature Review

Ethics of Carbon Disclosure

The review identifies persistent ethical weaknesses in carbon disclosure practices. Foley et al. (2024) claimed that the actual point is not the frameworks themselves but the way companies, frequently, that is, inconsistently, and occasionally, unethically, apply them. Thereupon, ESG disclosures have been doubted, more so when they are linked to net-zero objectives. Two issues are more prominent, namely the lack of transparency and non-uniform metrics. If these are absent, then it is impossible to cross-check reports from different companies or sectors (Widyawati, 2019). While ESG reporting has expanded, disclosures remain inconsistent, particularly for Scope 3 emissions, which are often incomplete or methodologically unclear. Data quality issues, double counting, and limited verification undermine comparability across firms and sectors (Hettler & Graf--Vlachy, 2023; Robinson et al., 2018).

Carbon offsets and renewable energy credits are frequently used to compensate for emissions, but are often poorly documented, increasing the risk of greenwashing (Sneideriene & Legenzova, 2025; Liu et al., 2023). ESG ratings do not always match real-world sustainability outcomes. This can happen because rules differ across regions, cultures approach sustainability differently, and companies vary in their openness about their practices (Lucarelli & Severini, 2024).

The ESG financial focus has been a significant factor in the ESG problem, where ethics are often marginalised. In such a case, firms can pursue a rapid increase in the financial side, leaving sustainability goals behind, so the gap between what firms say and what they actually do will increase in magnitude (Widyawati, 2019). Stakeholders need dependable, standard, measurable ways to see how each field is doing. Without these, it is hard to tell if ESG efforts are really changing things (Ilori et al., 2023). The absence of standardised reporting frameworks weakens stakeholder confidence and limits the ethical credibility of corporate climate claims. For instance, small enterprises are hindered by disorganised information and a shortage of funds, making it very difficult for them to complete the ESG report (Tsang et al., 2023; Suta et al., 2025).

Ethical Gaps in ESG Climate Metrics

Despite the growing number of ESG frameworks, significant ethical gaps remain across the design, reporting, and interpretation of ESG climate metrics. Variations in transparency and consistency across ESG measurements reduce their reliability and hinder meaningful comparison (Lucarelli & Severini, 2024; Widyawati, 2019). Many ESG ratings operate as opaque “black boxes,” offering limited transparency regarding methodological assumptions (Lucarelli & Severini, 2024). The dominance of financially oriented indicators further marginalises ethical and environmental substance.

Such a lack of clarity undermines the integrity of ESG metric outcomes, a practice in which companies exaggerate their environmental performance or selectively disclose only favourable information (Foley et al., 2024).

The cited literature documents that ESG is often understood solely from a financial perspective, with ethical issues overlooked (Landi & Sciarelli, 2019; Widyawati, 2019). This emphasis on financial performance can prioritise short–term gains over long-term sustainability, thereby reinforcing ethical gaps in ESG implementation (Chouaibi & Chouaibi, 2021). In addition, factors such as differing ESG regulatory standards, geographical distance, and cultural traditions, as well as varying corporate attitudes towards disclosure (Lucarelli & Severini, 2024; Suta et al., 2025). Lastly, the lack of standardised, verifiable, and sector-relevant metrics makes it nearly impossible for stakeholders to assess the actual value of corporate ESG engagement, leading to reduced commitment and trust (Ilori et al., 2023; Tsang et al., 2023).

The literature underscores the importance of standardisation in ESG metrics as a key priority. Lastly, industry-by-industry indicators show that ethical issues arising from ESG measures exhibit sectoral heterogeneity. Industries with high carbon content, such as oil and gas, face increased complexity in reporting Scope 3 emissions, and industries in water management still struggle to develop effective indicators of long-term sustainability performance (Christy et al., 2023; Sharaf-Addin, 2024).

Corporate Best and Worst Practices

Corporate reactions to ESG metrics and climate risk disclosure are incredibly varied, with clear examples of best and worst practices. Companies that incorporate ESG into their core business strategies, demonstrate moral leadership, and engage in dialogue with stakeholders are more likely to become sustainable in the long run and make a positive contribution to society (Eccles et al., 2014; Friede et al., 2015). Such organisations embed sustainability into their stewardship frameworks, thereby garnering more robust stakeholder confidence and achieving better alignment with international climate targets.

Compared to the above, worst practices are often associated with ESG controversies, superficial disclosures, and greenwashing, which not only weaken corporate credibility but also erode investor trust (Nirino et al., 2021; Elamer & Boulhaga, 2024). These controversies can significantly impact the company’s performance. Nevertheless, strong governance structures and well-established ESG systems may not only help alleviate these risks but also turn the company’s reputation problems into an opportunity (Elamer & Boulhaga, 2024).

Corporate governance and leadership diversity are important aspects of disclosure quality and ethical behaviour, as they inform an organisation’s accountability and transparency in its reporting (Hettler & Graf--Vlachy, 2023). Nevertheless, the relationship between ESG practices and financial performance remains difficult to untangle, depending on the circumstances. Some markets highly appreciate and reward sustainability initiatives, while in others they remain undervalued (Landi & Sciarelli, 2019). The results emphasise that real ESG integration cannot be limited to controlling reputation alone, but must be ingrained so deeply in the corporate culture that it becomes the norm, perpetuating change over time.

Best practices are observed in firms that embed ESG principles into governance structures, engage stakeholders, and align disclosures with long-term strategy. In contrast, worst practices are associated with symbolic reporting, selective disclosure, and ESG controversies. Strong governance mechanisms, including board diversity and independent oversight, play a critical role in mitigating ethical risks.

ESG Alignment with Climate Policy Goals

The alignment between ESG metrics and climate policy frameworks remains uneven. While references to the Paris Agreement and IPCC pathways are increasingly common, practical implementation varies widely across sectors and regions. Regulatory fragmentation and conflicting financial incentives limit effective translation of policy goals into corporate action (Kolk et al., 2008; Busch et al., 2016; Okereke et al., 2011). Nevertheless, a substantial gap exists between high-level, informative guidance and practical implementation; the extent of integration varies across sectors and regions (Doan & Sassen, 2020; Sullivan & Gouldson, 2017). In this regard, carbon-intensive sectors, such as oil and gas, generally face structural and regulatory challenges, with ESG implementation often delayed. At the same time, service-based sectors appear to be more adaptable in their climate-aligned reporting (Liesen et al., 2015). Additionally, the gradual incorporation of climate science into corporate strategies reflects the ongoing tension between short-term financial priorities and long-term sustainability imperatives (Widyawati, 2019; Velte et al., 2020).

The imposition of specifications, the necessity for disclosure, and the consistency of policy frameworks could improve comparability and reliability of ESG metrics not only for Sectors but also across countries (Busch et al., 2016; Vaio et al., 2025). In the absence of these, ESG risks become a mere symbolic gesture rather than a driver of substantial climate action. The working collaborative directions also encourage embedding evidence and objectives into corporate decision-making, ensuring that ESG reporting is not only compliant but also holds organisations to account (Ben-Amar et al., 2015; Hummel & Schlick, 2016). To sum up, the reconciliation of ESG activities with the global climate targets is not only a matter of regulations, but also an important avenue for corporate endurance and stakeholder loyalty in the long run.

Corporate Accountability to Net-Zero

Corporate net-zero goals are the basis of climate governance; however, the majority of those roadmaps remain vague, insufficient, or not fully aligned with scientific criteria. Research demonstrates that there is a gap, which, although recurrent, is gradually shrinking, between the emission-reduction targets announced by companies and their actual output, i.e., decarbonisation. The primary reasons for this gap are the non-exhaustive disclosure of information, the use of offsets, and weak accountability mechanisms (Anderson & Peters, 2016; Green, 2021). The moral aspects of the risk disclosures related to the transition are also barely touched upon, while the companies, in most cases, supply only fragments of data, these data being unfeasible to verify, and so they form the base for a lack of trust, too (Hettler & Graf--Vlachy, 2023; Borghei, 2021). The distrust is felt by the shareholders most when organisations issue containing leadership in climate action statements or otherwise giving a net-zero impression. However, any such progress cannot be checked or verified (Rogelj et al., 2021).

The results of a weak or delayed climate action will not just cause a bad public image to the company, but also will lead to various consequences such as regulatory penalties, financial risks, and a drop in the company’s competitiveness in those markets where the sustainability criteria are becoming more stringent (Krueger et al., 2020; Sato & Grubb, 2019). For effective accountability to be achieved, it is necessary to have strong governance structures that include different and independent boards, which are associated with better-quality sustainability disclosures and higher climate performance (Ben-Amar et al., 2015; Xu et al., 2025). Consistent regulatory frameworks, detailed standards for a particular sector, and the involvement of a third party for the assurance of the correctness of information are among those factors that are getting more and more attention as being necessary to eliminate the trust gap and to ensure that corporate emission reductions are in accordance with the Paris Agreement and national climate policy goals (Dietz et al., 2021; Kölbel et al., 2020). Thus, transparency and moral integrity, as key elements of corporate culture, are essential to making net-zero pledges not only believable but also achievable.

Corporate net-zero commitments frequently lack detailed transition pathways and measurable milestones. Heavy reliance on offsets, combined with limited third-party assurance, raises concerns about credibility. Weak accountability mechanisms expose firms to reputational and regulatory risks and undermine trust in climate leadership claims.

Discussion and Findings and Findings

The findings demonstrate that ESG metrics have evolved beyond compliance tools but remain ethically constrained by weak standardisation and assurance. If assurance mechanisms are ineffective, disclosures are at risk of being unreliable and prone to greenwashing (Vaio et al., 2025; Velte et al., 2020). Greenwashing risks persist, particularly in emissions reporting and offset use. Sectoral differences and governance quality significantly influence the credibility of disclosures. The review highlights apparent research gaps related to verification mechanisms, sector-specific metrics, and the integration of climate science into ESG frameworks.

The study found that ESG scores are evolving from a compliance tool to a significant influence on corporate environmental strategy, especially in emerging markets. The studied literature indicates that ESG metrics and climate risk reporting frameworks have made significant progress, but widespread ethical challenges remain. The lack of standardisation, openness, and strong assurance mechanisms leads to less credit being given to disclosing carbon and net-zero promises (Christy et al., 2023; Hettler & Graf--Vlachy, 2023; Vaio et al., 2025). Greenwashing, particularly in the issues of carbon offsets and renewable energy credits, is the primary concern that undermines stakeholder trust and the climate-friendly measures taken (Sneideriene & Legenzova, 2025; Liu et al., 2023). The adjustment of ESG metrics to help attain global climate policy goals is a work in progress, but it still faces challenges related to sectoral differences, data quality, and conflicting corporate priorities (Christy et al., 2023; Widyawati, 2019). The literature emphasises the necessity of standardising verification and deepening climate science knowledge in ESG strategies to ensure the ethical and practical actions towards net-zero targets. The thematic findings are shown in Table .

Table 1. Thematic Synthesis of Findings

| Theme | Key Issues | Representative Studies |

| Ethics of Carbon Disclosure | Incomplete and inconsistent Scope 1–3 emissions reporting; methodological challenges in emissions accounting and double counting; disclosure-related credibility risks | Foley et al. (2024); \textciteWidyawati (2019); \textciteHettler & Graf--Vlachy (2023); \textciteSneideriene & Legenzova (2025); \textciteRobinson et al. (2018) |

| Ethical Gaps in ESG Climate Metrics | Lack of convergence across ESG measurement frameworks; opacity in rating methodologies; dominance of financially oriented indicators; limited sector-specific metric relevance | Lucarelli & Severini (2024); \textciteLandi & Sciarelli (2019); \textciteChouaibi & Chouaibi (2021); \textciteTsang et al. (2023) |

| Corporate Best and Worst Practices | Role of ethical leadership, governance quality, and stakeholder engagement in shaping ESG performance; managerial practices that enhance or undermine credibility | Alhazemi (2025); \textciteAlmnadheh et al. (2025); \textciteElamer & Boulhaga (2024); \textciteNirino et al. (2021) |

| ESG Alignment with Climate Policy | Weak operationalisation of Paris Agreement and IPCC targets; regulatory fragmentation; sectoral variation in policy implementation; tensions between economic and climate objectives | Christy et al. (2023); \textciteMa et al. (2023); \textciteVelte et al. (2020); \textciteVaio et al. (2025); \textciteSullivan & Gouldson (2017) |

| Corporate Accountability to Net-Zero | Gaps between net-zero commitments and measurable outcomes; credibility of targets; reliance on offsets; verification and enforcement challenges | Borghei (2021); \textciteHettler & Graf--Vlachy (2023); \textciteRogelj et al. (2021); \textciteXu et al. (2025) |

| Cross-Cutting Themes and Sectoral Insights | System-wide need for standardisation and assurance; sector-specific measurement constraints; influence of governance structures and board characteristics on ESG quality | Vaio et al. (2025); \textciteSharaf-Addin (2024); \textciteChristy et al. (2023); \textciteXu et al. (2025) |

Theoretical Contribution

This review advances institutional and legitimacy theory by demonstrating how ESG disclosures function as legitimacy-seeking mechanisms rather than purely informational tools. Ethical weaknesses in ESG reporting reveal tensions between symbolic conformity and substantive climate action. By highlighting governance and assurance as mechanisms that enhance legitimacy, the study extends theoretical understanding of how institutions shape corporate climate behaviour. By highlighting moral loopholes, transparency challenges, and sector-specific variations, the articles contribute to institutional and legitimacy theory, demonstrating the impact of reporting on stakeholder trust and organisational accountability.

Moreover, the compilation illustrates that ESG structures may be able to trigger change and viability, especially when combined with the company’s long-term strategy and not considered merely as symbolic or reputational means. The view deepens the dialogue in the fields of sustainable accounting and climate change management, which is still ongoing, providing administrators, investors, and business leaders who want to enhance the trustworthiness and impact of climate-related disclosures with a broader range of implications.

Conclusion

This study shows that while ESG metrics play a central role in climate risk reporting, significant ethical challenges persist in disclosure quality, policy alignment, and net-zero accountability. Addressing these issues requires sector-specific standards, stronger governance structures, independent assurance, and regulatory harmonisation. Enhanced integration of climate science into ESG frameworks is essential to restore stakeholder trust and ensure that corporate net-zero commitments translate into meaningful climate action.

This review reveals that, although ESG metrics and climate risk reporting have undergone considerable evolution, serious ethical concerns persist, particularly in carbon disclosure, policy alignment, and net-zero accountability. Tackling these issues requires greater transparency, sector-specific standards, and independent assurance mechanisms. Strong corporate governance and diverse leadership are crucial to enhancing disclosure credibility and mitigating greenwashing. Ultimately, regulatory convergence and the deeper integration of climate science into ESG strategies are crucial for fostering trust and ensuring that corporate commitments translate into tangible climate action.

Supplementary Materials

Supplementary material for this article is available online via https://doi.org/10.51300/JSE-2026-164.

Funding Statement

No external funding was received

Conflict of Interest

The author declares that there is no conflict of interest regarding the publication of this paper.

References

- . A comparison between two main academic literature collections: Web of science and scopus databases. Asian Social Science, 9, 18--26.

- . Integrating ESG Framework with Social Sustainability Metrics: A Dual SEM-PLS Formative–Reflective Model Perspective. Sustainability, 17(6), 17--17. https://doi.org/10.3390/su17062566. CrossRef | Google Scholar

- . Enhancing ESG integration in corporate strategy: a bibliometric study and content analysis. International Journal of Law and Management, 67(2). https://doi.org/10.1108/ijlma-10-2024-0385. CrossRef | Google Scholar

- . The trouble with negative emissions. Science, 354(6309), 182--183. https://doi.org/10.1126/science.aah4567. CrossRef | Google Scholar

- . Corporate ESG reporting quantity, quality and performance: Where to now for environmental policy and practice?. Business Strategy and the Environment, 31(3). https://doi.org/10.1002/bse.2937. CrossRef | Google Scholar

- . Climate change sentiment, ESG practices and firm value: international insights. China Finance Review International, 15(3), 1--25. https://doi.org/10.1108/cfri-07-2024-0381. CrossRef | Google Scholar

- . Board Gender Diversity and Corporate Response to Sustainability Initiatives: Evidence from the Carbon Disclosure Project. Journal of Business Ethics, 142(2), 369--383. https://doi.org/10.1007/s10551-015-2759-1. CrossRef | Google Scholar

- . Corporate climate risk disclosure: Evidence from European companies. Sustainability Accounting, Management and Policy Journal, 12(5), 861--884. https://doi.org/10.1108/SAMPJ-09-2019-0339. CrossRef | Google Scholar

- . Sustainable development and financial markets: Old paths and new avenues. Business \& Society, 55(3), 303--329. https://doi.org/10.1177/0007650315570701. CrossRef | Google Scholar

- . Social and ethical practices and firm value: the moderating effect of green innovation: evidence from international ESG data. International Journal of Ethics and Systems, 37(3), 371--393. https://doi.org/10.1108/ijoes-12-2020-0203. CrossRef | Google Scholar

- . A dynamic framework to align company climate reporting and action with global climate targets. Business Strategy and the Environment, 33(4). https://doi.org/10.1002/bse.3635. CrossRef | Google Scholar

- . The valuation of corporate climate risk: Evidence from a meta-analysis. Review of Financial Studies, 34(8), 3501--3554. https://doi.org/10.1093/rfs/hhaa101. CrossRef | Google Scholar

- . The alignment of CSR and corporate governance practices with the Sustainable Development Goals: Evidence from the EU. Sustainability, 12, 8232--8232. https://doi.org/10.3390/su12208232. CrossRef | Google Scholar

- . ESG controversies and corporate performance: The moderating effect of governance mechanisms and ESG practices. Corporate Social Responsibility and Environmental Management, 31(4), 1--18. https://doi.org/10.1002/csr.2749. CrossRef | Google Scholar

- . Restoring trust in ESG investing through the adoption of just transition ethics. Renewable and Sustainable Energy Reviews, 199, 113404--113404. https://doi.org/10.1016/j.rser.2024.114557. CrossRef | Google Scholar

- . Corporate commitments to net-zero: Opportunities and limitations. Nature Climate Change, 11, 545--548. https://doi.org/10.1038/s41558-021-01038-2. CrossRef | Google Scholar

- . Corporate scope 3 carbon emission reporting as an enabler of supply chain decarbonization: A systematic review and comprehensive research agenda. Business Strategy and the Environment, 33(2). https://doi.org/10.1002/bse.3486. CrossRef | Google Scholar

- . ESG and Financial Performance: Aggregated Evidence from More Than 2000 Empirical Studies. Journal of Sustainable Finance \& Investment, 5(4), 210--233. https://doi.org/10.1080/20430795.2015.1118917. CrossRef | Google Scholar

- . The Impact of Corporate Sustainability on Organizational Processes and Performance. Management Science, 60(11), 2835--2857. https://doi.org/10.1287/mnsc.2014.1984. CrossRef | Google Scholar

- . Environmental, social, and governance disclosure in response to climate policy uncertainty: Evidence from US firms. Environment, Development and Sustainability, 26(2), 11013--11038. https://doi.org/10.1007/s10668-022-02884-5. CrossRef | Google Scholar

- . The relationship between sustainability performance and sustainability disclosure – Reconciling voluntary disclosure theory and legitimacy theory. Journal of Accounting and Public Policy, 35(5), 455--476. https://doi.org/10.1016/j.jaccpubpol.2016.06.001. CrossRef | Google Scholar

- . A Framework for Environmental, Social, and Governance (ESG) Auditing: Bridging Gaps in Global Reporting Standards. International Journal of Social Science Exceptional Research, 2(1), 1--15. https://doi.org/10.54660/ijsser.2023.2.1.231-248. CrossRef | Google Scholar

- . Can Sustainable Investing Save the World? Reviewing the Mechanisms of Investor Impact. Organization \& Environment, 33(4), 554--574. https://doi.org/10.1177/1086026620919202. CrossRef | Google Scholar

- . Corporate Responses in an Emerging Climate Regime: The Institutionalization and Commensuration of Carbon Disclosure. European Accounting Review, 17(4), 719--745. https://doi.org/10.1080/09638180802489121. CrossRef | Google Scholar

- . The importance of climate risks for institutional investors. Review of Financial Studies, 33(3), 1067--1111. https://doi.org/10.1093/rfs/hhz137. CrossRef | Google Scholar

- . Towards a more ethical market: the impact of ESG rating on corporate financial performance. Social Responsibility Journal, 15(1), 11--27. https://doi.org/10.1108/srj-11-2017-0254. CrossRef | Google Scholar

- . Does stakeholder pressure influence corporate GHG emissions reporting? Empirical evidence from Europe. Accounting, Auditing \& Accountability Journal, 28(7), 1047--1074. https://doi.org/10.1108/aaaj-12-2013-1547. CrossRef | Google Scholar

- . Why greenwashing occurs and what happens afterwards? A systematic literature review and future research agenda. Environmental Science and Pollution Research, 30(56), 12345--12367. https://doi.org/10.1007/s11356-023-30571-z. CrossRef | Google Scholar

- . Anatomy of the chimera: Environmental, Social, and Governance ratings beyond the myth. Business Strategy and the Environment, 33(5), 1--18. https://doi.org/10.1002/bse.3688. CrossRef | Google Scholar

- . Revisiting the role of firm-level carbon disclosure in sustainable development goals: Research agenda and policy implications. Gondwana Research, 117, 1--15. https://doi.org/10.1016/j.gr.2023.02.002. CrossRef | Google Scholar

- . Corporate controversies and company's financial performance: Exploring the moderating role of ESG practices. Technological Forecasting and Social Change, 162. https://doi.org/10.1016/j.techfore.2020.120341. CrossRef | Google Scholar

- . Climate Change: Challenging Business, Transforming Politics. Business \& Society, 51(1), 7--30. https://doi.org/10.1177/0007650311427659. CrossRef | Google Scholar

- . A Guide to Conducting a Systematic Literature Review of Information Systems Research. SSRN Electronic Journal, . https://doi.org/10.2139/ssrn.1954824. CrossRef | Google Scholar

- . Towards a universal carbon footprint standard: A case study of carbon management at universities. Journal of Cleaner Production, 172, 4435--4455. https://doi.org/10.1016/j.jclepro.2017.02.147. CrossRef | Google Scholar

- . Net-zero emissions targets are vague: three ways to fix. Nature, 591(7850), 365--368. https://doi.org/10.1038/d41586-021-00662-3. CrossRef | Google Scholar

- . International and sectoral dimensions of climate change mitigation: Trade, competitiveness, and carbon leakage. , 128, 317--329. https://doi.org/10.1016/j.enpol.2018.12.015. CrossRef | Google Scholar

- . Towards net-zero carbon emissions: A systematic review of carbon sustainability reporting based on GHG protocol framework. Environmental and Sustainability Indicators, 24. https://doi.org/10.1016/j.indic.2024.100516. CrossRef | Google Scholar

- . Greenwashing prevention in environmental, social, and governance (ESG) disclosures: A bibliometric analysis. Research in International Business and Finance, 74. https://doi.org/10.1016/j.ribaf.2024.102720. CrossRef | Google Scholar

- . Carbon performance and disclosure: A systematic review of governance-related determinants and financial consequences. Journal of Cleaner Production, 254, 120063. https://doi.org/10.1016/j.jclepro.2020.120063. CrossRef | Google Scholar

- . Towards Net-Zero Carbon Emissions: A Systematic Review of Carbon Sustainability Reporting based on GHG Protocol Framework. Environmental and Sustainability Indicators, . https://doi.org/10.1016/j.indic.2024.100516. CrossRef | Google Scholar

- . Dictionary-based assessment of European Sustainability Reporting Standard (ESRS) disclosure topics. Discover Sustainability, 6(1), 1--15. https://doi.org/10.1007/s43621-025-00123-4. CrossRef | Google Scholar

- . Environmental policy and competitive advantage: Why regulatory compliance is not enough. Business Strategy and the Environment, 26(3), 240--251. https://doi.org/10.1002/bse.1911. CrossRef | Google Scholar

- . Corporate controversies and company's financial performance: Exploring the moderating role of ESG practices. Technological Forecasting and Social Change, 158, 120118. https://doi.org/10.1016/j.techfore.2020.120118. CrossRef | Google Scholar

- . Bridging the gap: Building environmental, social and governance capabilities in small and medium logistics companies. Journal of Environmental Management, 330, 117099. https://doi.org/10.1016/j.jenvman.2023.117099. CrossRef | Google Scholar

- . A systematic literature review of socially responsible investment and environmental social governance metrics. Business Strategy and the Environment, . https://doi.org/10.1002/bse.2393. CrossRef | Google Scholar

- . Industry 4.0 integration with socio-technical systems theory: A systematic review and proposed theoretical model. Technology in Society, 61, 101248--101248. https://doi.org/10.1016/j.techsoc.2020.101248. CrossRef | Google Scholar

- . Board Diversity and Environmental Disclosure: A Review, Current Insights, and Emerging Trends. Sustainability, 17(2), 1234--1250.

- . Accounting and Accountability in the Transition to Zero-Carbon Energy for Climate Change: A Systematic Literature Review. . https://doi.org/10.1002/bse.4282. CrossRef | Google Scholar

About contributors

Shaji Thomas

Department of Commerce, Pavanatma College, Idukki, Kerala, India

India