Abstract

Sustainable finance models are most often built for contexts characterized by institutional stability, effective governance, and functioning capital markets. In fragile states, such conditions are often absent. This paper revisits sustainable finance through the case of Lebanon, where the post-2019 financial collapse rendered conventional instruments, such as ESG frameworks, green bonds, and sustainability-linked loans, difficult to implement and contextually irrelevant. Drawing on literature regarding sustainable finance, degrowth and post-growth economics, and the political economy of fragility, the paper proposes a conceptual framework for Agile Sustainable Finance: a model that explains how financial practices oriented towards sustainability can persist despite institutional collapse with agility operating as the mediating capability. The model positions agility as the central capability enabling households, firms, and communities to reorganize financial life amid institutional erosion, liquidity shortages, and involuntary degrowth. It highlights how informal credit systems, remittances, community financing, and decentralized energy solutions become essential tools for resilience and ecological sufficiency in collapsed economies. By reframing finance as a mechanism for survival, redistribution, and basic sustainability rather than growth, this conceptual study offers a theoretical model that bridges domains that rarely intersect: sustainable finance and fragile-state dynamics.

Introduction

Conventional approaches to sustainable finance often rest on a set of shared assumptions: functioning institutions, reliable governance, and economies oriented towards growth (Boccaletti & Gucciardi, 2025).When these assumptions fail, the relevance of mainstream sustainable finance frameworks is fundamentally challenged.In countries experiencing severe systemic breakdowns, such as Lebanon, these models begin to lose relevance.Since late 2019, Lebanon has undergone the near-total collapse of its banking sector, uncontrolled inflation, and a widespread loss of public trust in both state and financial institutions

.In this environment, traditional sustainable finance tools, like ESG frameworks, green bonds and other types of sustainability-linked loans are not only difficult to access but increasingly disconnected from the country’s urgent needs, as national priorities shift toward economic stabilization and social resilience.These sustainability tools rely on institutional foundations that have eroded in such fragile environments.Recent research on Lebanon’s agricultural and rural sectors highlights how structural vulnerabilities, declining institutional capacity, and widespread poverty constrain the country’s ability to implement sustainability-oriented policies (Roberts & Naimy, 2023).

This paper introduces a conceptual reframing of sustainable finance, tailored to fragile contexts, that does not rely on assumptions of institutional strength or continuous growth.Taking Lebanon as an illustrative example, it proposes a conceptual framework that shifts the focus to resilience, local agency, and ecological sufficiency.In such settings, finance does not primarily serve to allocate capital efficiently or maximize returns

.Rather, it becomes a mechanism through which households and communities endure, adapt, and sustain basic economic and social functions in the absence of effective state support.Drawing on degrowth and post-growth literature, the paper argues that sustainable finance must remain meaningful even under conditions of economic contraction or systemic collapse (Hickel, 2021).

Despite the rapid expansion of sustainable finance research, limited attention has been paid to how such frameworks operate when institutional stability, governance capacity, and growth can no longer be assumed.This constitutes a critical conceptual gap: what sustainable finance becomes when formal financial mechanisms cease to function.

To address this gap, the paper proposes the concept of Agile Sustainable Finance, theorizing agility as a mediating capability between institutional breakdown and sustainability-oriented outcomes in fragile economies.The study develops a conceptual framework grounded in interdisciplinary literature and illustrates its relevance through the Lebanese context.

Aims and Contributions

The primary aim of this paper is to propose a conceptual framework for Agile Sustainable Finance: a model that explains how sustainability-oriented financial practices can persist despite institutional collapse, with agility operating as the mediating capability that enables such persistence. Using Lebanon as an illustrative context, the framework clarifies how financial life continues and reorganizes when formal financial mechanisms fail.

This paper makes four main contributions:

-

Conceptual reframing: It reframes sustainable finance beyond growth-oriented and institution-centric models by conceptualizing sustainability as grounded in resilience, local agency, and ecological sufficiency in fragile contexts.

-

Agility as a mechanism: It theorizes agility as a mediating capability linking institutional breakdown to sustainability-oriented outcomes, explaining how households, firms, and communities adapt financial practices under conditions of crisis and involuntary degrowth.

-

Bridging literatures: It bridges sustainable finance with the political economy of fragile states, addressing a gap in both literatures regarding how financial life persists through informal, adaptive, and community-based mechanisms when formal institutions collapse.

-

Framework for future research and policy: It provides a structured conceptual model and propositions that can guide future empirical research and inform policy interventions aimed at supporting sustainability and resilience in fragile and crisis-affected economies.

Literature Review

Rethinking Sustainable Finance Beyond the Growth Paradigm

Sustainable finance refers to financial decisions and activities that aim to support both environmental protection and social well-being. It involves integrating ESG standards into investment and lending practices to encourage long-term economic resilience and social responsibility (Bandna et al., 2025). It includes instruments such as green bonds, social and impact bonds, and sustainability-linked loans, designed to direct capital toward sustainability-focused projects. The market for these instruments has shown significant growth, driven by global policy initiatives, investor demand for responsible assets, and the rising recognition of sustainability as a driver of financial resilience (Cheng et al., 2022; Kim et al., 2025)

Although research on sustainable finance has grown rapidly, it generally rests on the assumption that financial innovation can advance both economic growth and sustainability goals. However, evidence shows that even in stable markets, socially responsible investment remains constrained by behavioral contradictions, where investors often prioritize financial returns over ethical motives, revealing the fragility of voluntary, values-based finance models (Heimann & Lobre-Lebraty, 2019). Recent work on behavioral interventions in responsible finance further shows how difficult it is to align financial decision making with sustainability objectives, even when investors are “nudged” toward more responsible choices (Gajewski et al., 2023). Similarly, volatility in ESG-linked assets and green-finance instruments has been shown to increase under uncertainty, revealing the fragility of sustainability-oriented finance even in markets that are otherwise functional (Arouri et al., 2025). These behavioral and market challenges point to a larger issue: the assumptions underpinning sustainable finance may not hold up in fragile or unstable environments.

While mainstream sustainable finance frameworks emphasize capital allocation toward environmental and social objectives, they implicitly rely on functioning institutions, regulatory enforcement, credible reporting systems, and stable financial intermediation. Under conditions of institutional breakdown, these frameworks fail through identifiable mechanisms rather than normative shortcomings. These mechanisms include governance failures, marked by the erosion of regulatory authority and enforcement capacity; accountability failures, reflected in the collapse of trust, reporting credibility, and contractual enforceability; quality failures, arising from the deterioration of financial and physical infrastructures required to support sustainable investment; and information failures, characterized by fragmented data, unreliable metrics, and misaligned socio-technical systems (Murray & Dollery, 2005; Zhang & Liao, 2025). As these mechanisms weaken, core sustainable finance instruments, such as ESG metrics, green bonds, and sustainability-linked finance, lose operational meaning. This suggests that the limitations of sustainable finance in fragile contexts stem not from a lack of sustainability intent, but from the institutional conditions required for its instruments to function.

Only a limited body of work directly questions the growth dependence built into these financial tools or considers how sustainable finance might function in fragile or stagnant economies (Ramos Farroñán et al., 2025). Addressing this gap calls for a re-examination of sustainable finance beyond conventional growth assumptions. The following section explores how post-growth and degrowth theories challenge these growth assumptions and offer alternative paradigms for sustainable finance.

Post-growth and Degrowth Economics

While sustainable finance seeks to align financial systems with ESG objectives, post-growth and degrowth theories question whether such alignment is possible when economic systems depend on continuous growth.

Post-growth and degrowth economics have emerged as influential frameworks challenging the assumption that continuous economic growth is both achievable and desirable. Post-growth economics calls for a reorientation of economic priorities from GDP maximization toward enhancing human well-being, social equity, and ecological resilience (Jackson, 2009; Kallis et al., 2025). Degrowth, while sharing these core principles, adopts a more explicit position by advocating a deliberate and equitable downscaling of production and consumption to operate within planetary boundaries and to address entrenched global inequalities (Schmelzer et al., 2022; Hickel, 2021). Together, these perspectives seek to redefine what economic progress means, focusing on sufficiency, local agency and ecological sustainability, rather than mere expansion.

Building on these perspectives, Durand et al. (2023) extend the post-growth and degrowth debate by addressing a long-standing gap: how to plan economic activity beyond the pursuit of growth. Their work introduces a framework for “planning beyond growth,” emphasizing democratic, multi-level, and ecologically informed decision-making, where financial and institutional mechanisms serve collective needs rather than market-driven expansion. This viewpoint reinforces the idea that sustainable finance must evolve toward locally grounded, adaptive, and context-sensitive models capable of balancing social priorities with ecological limits.

Degrowth and post-growth perspectives contribute to finance not merely by advocating “less growth,” but by fundamentally rethinking the purpose, governance, and normative foundations of economic activity under conditions of ecological constraint and social inequality (Alexander, 2011). Rather than treating finance as a neutral mechanism for capital accumulation, these frameworks repoliticize financial relations by foregrounding questions of distribution, democratic control, and collective well-being. Conceptually, they shift attention from efficiency and return maximization toward sufficiency, care, and the maintenance of essential social and ecological functions. In financial terms, this implies reorienting investment away from growth-dependent performance metrics toward supporting livelihoods, basic services, and community-based provisioning systems that remain viable under conditions of stagnation or contraction. Post-growth perspectives further challenge the centrality of profit maximization in financial decision-making, arguing that sustainability requires a redefinition of the relationship between purpose, investment, and ownership rather than incremental efficiency gains within existing financial logics (Hinton, 2020). Importantly, degrowth and post-growth perspectives also distinguish between voluntary and involuntary contraction, thereby providing conceptual tools to analyze financial practices in contexts where economic decline is imposed rather than planned. This makes them particularly relevant for fragile and crisis-affected economies, where finance must operate without the expectation of recovery-led growth.

This conceptual foundation aligns closely with the central argument of the present study: that in fragile economies such as Lebanon, financial systems must be restructured around sustainability, local agency, and resilience rather than growth. Integrating the “planning beyond growth” approach into the financial scope provides a theoretical basis for sustainable finance without growth, where capital allocation, regulation, and risk management are designed to support social and ecological objectives rather than GDP expansion. This approach highlights the importance of strong, adaptive institutions capable of reconciling economic activity with social and ecological goals. Yet, in many fragile economies, precisely these institutional capacities are underdeveloped, leaving them highly exposed to crises and systemic shocks.

Fragile and Crisis Economies: The Limits of Mainstream Finance

Fragile economies are defined by deep structural weaknesses that leave them highly vulnerable to shocks and systemic crises. These weaknesses often result from a mix of macroeconomic instability, weak institutions, and underinvestment in human capital, thereby eroding resilience and social cohesion (Elbadawi et al., 2021). A defining feature of these economies is their economic fragility itself. Persistent inflation, unsustainable public debt, and large external deficits limit fiscal and monetary independence, leaving them vulnerable to speculation and external pressure (Thompson, 2020).

Institutional quality is equally crucial. As Stewart & Chowdhury (2025) note, strong institutions, particularly in governance, are central to how effectively countries can respond to crises. Weak governance tends to undermine policy credibility, weaken banking systems, and limit the ability to mobilize domestic resources, leaving economies more exposed when shocks occur. Financial instability in fragile economies tends to deepen during crises due to limited institutional capacity and pro-cyclical behavior. In such settings, credit and investment patterns become highly volatile, amplifying social vulnerabilities. Conventional tools, such as counter-cyclical fiscal policy or central bank interventions, are often unavailable or ineffective. This highlights the limits of mainstream financial frameworks in these contexts. As Froemel & Paczos (2024) note, fiscal retrenchment during downturns worsens social inequality, particularly when sovereign risk is high and public trust is low.

While fragility and political economy literatures have extensively examined state failure, governance breakdown, and aid dependence, they often under-theorize how financial life continues in practice when formal systems collapse. Informal financial mechanisms, such as community-based savings arrangements, remittance networks, trust-based credit, and hybrid cash-digital practices, are frequently treated as residual, temporary, or deficient substitutes for formal finance rather than as central organizing features of economic survival. Evidence from financial diaries further illustrates how informal lending functions as a day-to-day social safety net, allowing financially vulnerable households to manage short-term liquidity shocks when formal financial instruments are inaccessible (Biosca et al., 2020). Recent scholarship further challenges the assumption that informality constitutes a barrier to financial inclusion, showing instead that certain forms of informal finance can play a developmental or complementary role alongside formal financial systems (Ma, 2025). This omission obscures the sociocultural foundations of financial coordination in fragile contexts, where trust, social norms, and informal institutions frequently replace legal enforcement and regulatory oversight. As a result, fragility analyses tend to overlook how households and communities actively adapt financial practices to manage liquidity, risk, and basic provisioning under conditions of systemic breakdown. Recognizing informal finance as an integral component of financial life, rather than a deviation from it, is therefore essential for understanding how economic activity persists, adapts, and sustains livelihoods in fragile and crisis-affected economies.

These dynamics underscore the urgency of exploring financial alternatives that are not dependent on institutional strength, market stability, or economic growth. In many post-collapse or fragile economies, informal systems of finance including remittances, mutual aid networks and community credit systems, become primary means of survival (Castro-Cosío, 2023; van Asselt et al., 2025). Rather than optimizing markets, finance in these contexts functions as a tool for resilience, resource sharing, and community cohesion. Recognizing and theorizing these informal mechanisms is essential to developing a sustainable finance model that is relevant to fragile and crisis-prone economies like Lebanon.

The review of sustainable finance, post-growth theory, and fragile economies reveals a clear conceptual gap: existing frameworks assume functioning institutions, monetary stability, and access to capital markets. Yet, in collapsed systems, finance continues through informal, community-based, or resilience-driven mechanisms that remain largely untheorized. Addressing this gap requires a redefinition of finance not as a driver of growth but as a mechanism of survival, equity, and ecological balance. Building on this foundation, the next section develops a conceptual framework for sustainable finance without growth, grounded in the lived realities of post-collapse economies such as Lebanon.

In this study, Agile Sustainable Finance is not proposed as a new category of sustainable finance nor as a resilience-finance framework. Rather, it is conceptualized as a bridging framework that links short-term resilience practices with longer-term sustainability objectives, with agility operating as the mediating capability between the two in fragile economic contexts.

Following this conceptual positioning, agility is introduced as a key building block for rethinking sustainable finance in fragile economies. Inspired by the concept of resilient agility (Gölgeci et al., 2019), the term here takes on a different meaning from how it is used in stable markets. It is not about institutional performance or streamlined innovation. Instead, it reflects how people and communities, working both inside and outside formal systems, adjust, reorganize, and carry on in the face of disruption and uncertainty.

In places where banking collapses, inflation soars, and governance fails, agility shows up in practical, ground-level ways: informal lending circles, community cooperation, shared risk and creative use of limited resources. These are not mechanisms for maximizing profits, but rather for maintaining continuity and withstanding disruption. Agility, then, becomes less about market efficiency and more about human and community resilience. It is how people navigate broken systems and find new paths when old structures no longer work. By bringing resilient agility into the conversation on sustainable finance, we gain a vocabulary for these adaptive strategies, and begin to see how financial life continues, even without growth, institutions, or stability.

Mechanism and Propositions: Agility as a Mediating Capability

In fragile and post-collapse economies, institutional breakdown alters the conditions under which financial systems operate. The erosion of regulatory capacity, monetary stability, and public trust disrupts formal financial intermediation and constrains access to conventional sustainability-oriented instruments. In this context, agility is conceptualized as a mediating capability that links conditions of institutional failure to the persistence of basic resilience and sustainability outcomes.

Conceptual Mechanism (X →Agility →Y)

In this framework, X refers to conditions of systemic fragility, including institutional collapse, liquidity shortages, loss of trust in formal financial systems, and macroeconomic instability. These conditions undermine the functionality of formal sustainable finance mechanisms and shift financial activity toward informal, community-based, or hybrid arrangements.

Agility operates as the mediating capability through which households, communities, and local economic actors adapt financial practices in response to these disruptions. It reflects the capacity to reorganize financial coordination rapidly, recombine formal and informal mechanisms, and mobilize social networks to maintain essential economic and social functions under conditions of uncertainty.

Y refers to the persistence of core outcomes that are consistent with sustainability in fragile contexts. These outcomes are not defined in terms of growth or market efficiency, but rather in terms of (i) short-term resilience outcomes, such as liquidity management and risk sharing; and (ii) longer-term sustainability-oriented outcomes, including basic provisioning, social cohesion, and ecological sufficiency.

Observable Indicators of Agility

Agility is observable through concrete financial practices that emerge or intensify when formal systems fail. These include, but are not limited to:

-

increased reliance on informal savings and credit arrangements(e.g., ROSCAs and community lending circles);

-

expanded use of remittance networks as liquidity and risk-sharing mechanisms;

-

the emergence of hybrid cash–digital financial practices, including mobile money layered onto informal systems;

-

localized, community-based provisioning systems, such as mutual aid networks or decentralized energy and resource-sharing arrangements.

These practices illustrate how financial life adapts dynamically rather than collapsing entirely when institutional support erodes.

Propositions

Based on this conceptual mechanism, the following propositions are advanced to guide future empirical research:

-

P1:

Institutional collapse and macroeconomic instability increase reliance on informal and hybrid financial mechanisms.

-

P2:

Higher levels of financial agility are associated with improved short-term resilience outcomes, including liquidity smoothing and household-level risk sharing.

-

P3:

Financial agility mediates the relationship between institutional breakdown and the persistence of sustainability-oriented practices, such as basic provisioning, social cohesion, and ecological sufficiency.

-

P4:

In fragile economies, sustainability outcomes are more likely to persist where agile financial practices successfully integrate informal coordination with residual or adapted formal mechanisms.

Together, these propositions position agility not as an abstract attribute, but as a causal mechanism through which financial systems continue to function and sustain livelihoods under conditions of fragility. They also provide a structured basis for future empirical testing across different crisis-affected and post-collapse economic contexts.

Conceptual Framework for Resilient Finance in Fragile Economies

This section outlines the conceptual methodological approach used to develop the framework, before presenting the resulting conceptual model.

In light of systemic constraints associated with institutional breakdown and involuntary degrowth, this paper introduces agility as a key conceptual building block for rethinking sustainable finance in fragile economies. Inspired by the notion of resilient agility, but adapted to crisis contexts, agility is conceptualized here as a mediating capability rather than a performance attribute. This conceptual approach guides the development of the framework presented below.

Conceptual Approach and Rationale

This conceptual framework is grounded in a synthesis of three strands of scholarship: sustainable finance, degrowth and post-growth theory, and the political economy of fragile states. Following an integrative conceptual approach (MacInnis, 2011) , it reinterprets the purpose and functioning of finance under conditions of institutional erosion and macroeconomic breakdown. Instead of viewing finance as a mechanism for capital accumulation and economic expansion, the framework reframes it as a system oriented toward resilience, redistribution, and ecological balance. This shift provides the foundation for analyzing how financial practices evolve in fragile economies and why traditional sustainable-finance instruments become inapplicable when institutional structures collapse.

Dual Contexts of Financial Functioning

The first step in developing the framework is recognizing that financial systems operate differently depending on the macroeconomic environment. In stable, growth-driven economies, institutional capacity, regulatory predictability, and functioning markets provide the conditions necessary for conventional sustainable finance. Instruments such as green bonds, sustainability-linked loans, and ESG-based investment mechanisms rely on regulatory oversight, credible reporting systems, and access to capital markets. Within these settings, finance is designed to support long-term planning, investment, and innovation.

By contrast, fragile and crisis-affected economies function under a radically different set of conditions. Institutional weakness, severe liquidity shortages, and declining public trust reshape financial behavior and make long-term planning nearly impossible. The macroeconomic trajectory in such settings tends to move toward involuntary degrowth, characterized by shrinking output, reduced consumption, and declining formal investment. As institutions weaken and markets contract, financial actors are not able to rely on formal tools. This divergence reveals a key blind spot in mainstream sustainable finance theory: most frameworks were built for stable environments and fail to account for situations where institutions are weak or altogether absent.

Degrowth and the Inaccessibility of Formal Financial Tools

In fragile settings, involuntary degrowth is not a policy decision, but a structural outcome driven by crisis dynamics. The decline of institutional capacity leads to the breakdown of formal channels through which sustainable finance mechanisms typically operate and depend on. Access to credit becomes limited, capital markets lose relevance, and international financing becomes harder to secure. Meanwhile, regulatory compliance, reporting systems, and long-term ESG commitments become increasingly difficult to maintain. Empirical evidence shows that even in more stable economies, sustainability-linked financial instruments become highly volatile when institutions weaken or when macro uncertainty rises (Arouri et al., 2025). The inaccessibility of these formal tools does not eliminate the need for sustainable finance but reveals the mismatch between mainstream sustainable finance instruments and the realities of economies facing collapse. Because these tools depend on stability, even well-established markets exhibit disrupted financial behavior when uncertainty rises. Evidence from GCC stock markets shows that climate-policy uncertainty significantly weakens financial linkages and reduces market predictability (Arouri et al., 2025). In fragile economies, where uncertainty is far more severe and persistent, this instability becomes structural rather than episodic. Where institutions can no longer support structured financing, economic actors turn toward alternative, improvised, or informal mechanisms to meet basic needs and preserve essential functions.

Agility as the Mediating Capability

Agility emerges as the central mediating capability that allows financial practices to adapt to volatility and institutional collapse. In fragile economies, agility refers to the ability of households, businesses, and communities to adjust rapidly to shocks, reorganize in the face of uncertainty, and develop improvised solutions when formal structures fail. Agility replaces stability as the primary organizing principle. Similar patterns are documented in other fragile contexts, where institutional erosion forces organizations to rely on adaptability, informal coordination, and locally embedded capabilities to sustain operations (Fares & Valax, 2024).

A similar adaptive logic is observed in cooperative financial institutions, where frontline actors reframe performance systems to balance social and financial goals under uncertainty (Bénet et al., 2024). This supports the broader argument that agility involves not just structural improvisation, but also interpretive flexibility when navigating unstable environments.

Comparable dynamics are also observed in more stable economies when uncertainty rises sharply; for example, climate-policy uncertainty has been shown to disrupt financial relationships and weaken the effectiveness of formal market signals, underscoring the importance of adaptive responses (Arouri et al., 2025). Agility enables agents to navigate between formal and informal systems, devise low-cost local solutions, repurpose financial tools, and operate in short adaptive cycles instead of long-term plans. Within this framework, agility forms the conceptual bridge that links conventional sustainable finance principles with the realities of fragile economies. Without agility, sustainable finance remains tied to institutional structures that no longer exist. With agility, they become adaptable, localized, and applicable in crisis contexts.

The transition toward sustainable outcomes in volatile and institutionally constrained environments increasingly depends on the interaction between technical capabilities and adaptive financial mechanisms rather than on formal innovation systems alone. Recent work highlights that environmental innovation and technical cooperation can support sustainability trajectories even where institutional frameworks are weakened or undergoing stress (Ullah & Lin, 2025; Ullah & Lin, 2025). In such contexts, the combination of green finance instruments and decentralized renewable energy initiatives facilitates adaptive financial practices that allow sustainability-oriented activities to persist under resource constraints (Ullah & Lin, 2025). This literature suggests that human capital, when mobilized through localized green initiatives and flexible policy support, can contribute to bridging institutional breakdown and community-level ecological sufficiency, reinforcing the adaptive logic underlying Agile Sustainable Finance (Ullah & Lin, 2025).

Note :This model illustrates how Agile Sustainable Finance emerges when institutional collapse and involuntary degrowth render conventional sustainable financial instruments inapplicable. Agility functions as the mediating capability that enables households, communities, and local agencies to sustain financial and ecological resilience through informal mechanisms. The model reframes finance as a tool for survival, redistribution, and ecological balance rather than economic growth.

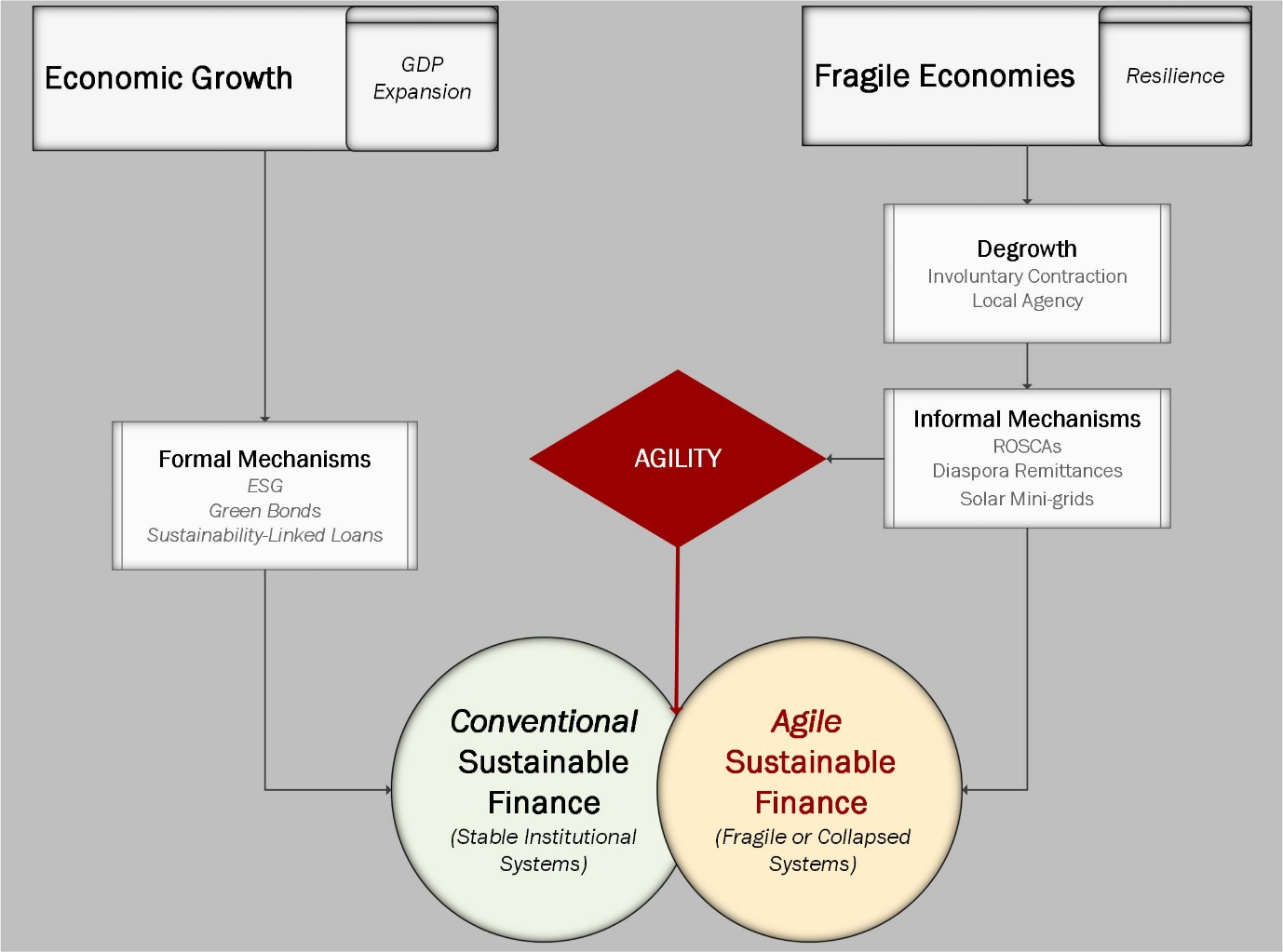

Reading the Conceptual Model: Resilience, Sustainability, and Agility

Figure 1 provides a visual synthesis of the conceptual framework developed in this paper and clarifies how financial systems function under contrasting institutional conditions. The model distinguishes between stable, growth-oriented economies and fragile or collapsed economies, and illustrates how sustainable finance operates differently across these contexts.

On the left-hand side of the figure, economic growth and GDP expansion characterize environments with functioning institutions, regulatory enforcement, and access to capital markets. Under these conditions, sustainable finance relies primarily on formal mechanisms, including ESG integration, green bonds, and sustainability-linked loans. These instruments depend on institutional stability, credible reporting, and long-term planning horizons, and together form what the model labels conventional sustainable finance.

The right-hand side of the figure represents fragile economies, where institutional collapse, macroeconomic instability, and loss of trust undermine formal financial intermediation. In these contexts, economic contraction is typically involuntary and aligns with degrowth dynamics driven by crisis rather than policy choice. As formal mechanisms become inaccessible or ineffective, financial coordination increasingly shifts toward informal mechanisms, such as rotating savings and credit associations (ROSCAs), diaspora remittances, decentralized energy systems, and hybrid cash–digital practices.

At the center of the model, agility is positioned as the mediating capability linking these informal and hybrid mechanisms to financial outcomes. Agility captures the capacity of households, communities, and local actors to rapidly reorganize financial practices, recombine available resources, and maintain coordination under conditions of uncertainty. It is through agility that financial life continues when institutional support erodes, allowing adaptive practices to emerge rather than complete financial breakdown.

A key conceptual distinction highlighted by the model is the relationship between resilience and sustainability. In fragile economies, resilience refers to short-term capacities to absorb shocks, manage liquidity, and maintain basic economic functioning. Sustainability, by contrast, refers to the longer-term persistence of social provisioning, community cohesion, and ecological sufficiency. Rather than being interchangeable or competing concepts, resilience is treated here as a necessary precondition for sustainability in fragile contexts. Without resilience, sustainability outcomes cannot persist; without sustainability, resilience remains confined to short-term survival.

Within this framework, Agile Sustainable Finance is not proposed as a new category of sustainable finance nor as a purely resilience-focused approach. Instead, it is conceptualized as a bridging framework that links short-term resilience practices to longer-term sustainability objectives under conditions of institutional fragility. Agility mediates this transition by enabling informal and adaptive financial mechanisms to support not only survival, but the continued provision of essential social and ecological functions in the absence of growth and institutional stability.

From Conventional to Agile Sustainable Finance

The transformation from conventional sustainable finance models to “Agile Sustainable Finance”is not a rejection of sustainability principles, but a reconfiguration of how these principles are applied. Traditional models rely on stable markets, institutional trust, and formal oversight mechanisms. Agile Sustainable Finance, by contrast, is rooted in decentralized, adaptive, and community-based practices that are capable of operating under extreme uncertainty. It is characterized by fluid strategies, improvisation, and local agency. In fragile settings, sustainability therefore emerges in forms that are not formally recognized by mainstream finance: neighborhood-funded solar installations, informal rotating savings groups, diaspora-supported resilience projects, hybrid cash-digital micro transactions, and local circular-economy practices.

Rotating savings and credit associations (ROSCAs) have long served as informal financial mechanisms that enhance resilience and social development in underprivileged communities (Zambrano et al., 2023). Community-owned solar systems, such as solar mini-grids, have demonstrated resilience and replicability when managed through locally driven governance structures (Katre et al., 2019). Diaspora-supported resilience projects, such as collective remittance initiatives to improve health and social infrastructure, have been shown to increase community resilience in places like Niaogho, Burkina Faso (Meyer & Strohle, 2023). Hybrid cash–digital micro transactions are also emerging, as mobile platforms increasingly support informal saving groups and bridge gaps between formal and informal finance (Wambua & Wamuyu, 2020). These activities preserve environmental balance and social continuity, but they do so through mechanisms that differ fundamentally from conventional financial instruments. Agile Sustainable Finance captures this shift and offers a conceptual pathway for understanding how sustainability persists in environments where formal systems have collapsed.

Lebanon as a Conceptual Lens: Illustrating Agile Sustainable Finance

Lebanon provides a compelling illustration of Agile Sustainable Finance in action. It is important to emphasize that this paper does not present an empirical case study of Lebanon, nor does it seek to establish causal relationships or test hypotheses using country-level data. Rather, Lebanon is employed as an illustrative conceptual lens to motivate, exemplify, and ground the proposed framework of Agile Sustainable Finance in a real-world context of institutional collapse and involuntary degrowth. The references to banking failure, informality, remittances, and decentralized energy systems are therefore intended to demonstrate the relevance and plausibility of the conceptual arguments, not to provide empirical validation. Lebanon serves as an analytically useful setting through which the mechanisms discussed earlier can be made concrete, without claiming generalizability or causal inference. Recent research shows that Lebanese farmers operate within severe structural constraints, including limited credit, weak institutions, and declining state support, which reinforces the need for community-based adaptive financial practices (Roberts & Naimy, 2023). Since 2019, Lebanon has experienced the collapse of its banking system, frozen deposits, unofficial capital controls, and a breakdown in trust between citizens and financial intermediaries. Public confidence in Lebanon’s financial system has deteriorated sharply. Years of financial mismanagement, regulatory opacity, and the collapse of trust in monetary authorities have led many citizens to perceive the banking system as deceptive or extractive. This erosion of trust is not merely a symptom of collapse – it is also a catalyst for financial innovation. As formal systems lose credibility, communities turn to informal mechanisms that are more responsive, transparent, and rooted in local agency (Sawaya et al., 2023). These adaptive practices do not only reflect economic necessity but also carry political significance.

As Helou (2022) argues, the widespread turn toward informality in Lebanon is not just a survival mechanism, it represents a form of implicit resistance to the sectarian political-economic model that underpinned the crisis. Informal financial practices such as currency substitution, parallel markets, and community-based exchanges allow citizens to reclaim a degree of economic agency, challenge state authority over monetary governance, and redefine the social contract.

Remittances play a particularly important role within this ecosystem of adaptive finance. As Ghandour et al. (2025) show, remittance inflows have historically helped reduce income inequality in Lebanon by supplementing household income, especially in the absence of inclusive state support. However, their redistributive effect was shown to weaken during the post-2019 crisis period, as the function of remittances shifted from long-term support to short-term survival. This dynamic reinforces a key principle of Agile Sustainable Finance: adaptive financial mechanisms can be powerful tools for social stability, but their function and impact can evolve dramatically in the context of systemic collapse. Moreover, the finding that financial development can dampen the redistributive impact of remittances suggests that formal financial expansion, without inclusion and institutional trust, may hinder rather than enhance sustainability in fragile economies.

Decentralized renewable energy systems offer another powerful illustration of agile sustainability finance in action. In a comparative case study conducted in Lebanon, Herez et al. (2025) demonstrate that hybrid photovoltaic-thermal (PVT) systems significantly outperform traditional solar PV in energy efficiency, economic returns, and environmental impact. With fast payback times and significant carbon reductions, these systems have become more than energy alternatives, they are community-level financial solutions. In contexts where public infrastructure collapses, such systems help communities manage fuel shortages, inflation, and currency instability through locally controlled, low-cost investments.

Together, these community-driven responses, including solar-based energy systems, remittance-backed coping strategies, or informal credit networks, reflect a broader shift in how finance operates when formal structures fail. Conventional sustainable-finance instruments, such as green loans and ESG-linked financing, lose relevance in collapsed contexts. In the vacuum left by institutional breakdown, communities have developed agile, decentralized financial practices to meet urgent economic and ecological needs. Lebanon thus illustrates not simply a workaround to system failure, but a real-time experiment in how sustainability can persist outside traditional frameworks, offering a conceptual foundation for rethinking sustainable finance in fragile and crisis-affected economies through the lens of agility.

Contribution of the Framework

This conceptual framework contributes to sustainable finance scholarship by directly challenging the dominant assumptions behind most current models – namely, that financial systems operate in growth-oriented, institutionally stable environments. It introduces agility as a foundational capability that enables sustainability to persist even under conditions of systemic fragility. In this reframing, finance is no longer viewed as a tool of economic expansion, but as a mechanism for maintaining resilience and socio–economic continuity in the face of institutional collapse. By integrating the dynamics of involuntary degrowth, institutional collapse, and adaptive financial behavior into a unified model, the framework offers a fresh perspective for analyzing financial systems in crisis-affected economies. Importantly, it also opens promising avenues for empirical inquiry and policy innovation aimed at enhancing resilience in settings where conventional sustainable financial instruments and institutions have lost functionality.

Discussion and implications

The conceptual framework developed in this paper repositions sustainable finance by moving past its dependence on institutional stability and growth-oriented assumptions. Through the introduction of Agile Sustainable Finance, it demonstrates that sustainability not only persists but can also adapt and evolve under conditions of institutional collapse. This shift carries significant implications for theory, policy, and practice, particularly in economies experiencing protracted fragility and systemic dysfunction.

Theoretical Implications

This framework advances sustainable-finance theory by challenging the assumption that sustainability requires functioning institutions, market stability, and formal regulatory structures. Fragile economies reveal that financial life continues even when these conditions collapse, relying instead on informal, adaptive, and community-based mechanisms. Recognizing these alternative financial behaviors broadens the scope of sustainable finance and highlights the need for models that do not rely on growth or institutional capacity.

The incorporation of agility also contributes to post-growth and degrowth scholarship. While these literatures typically explore intentional transitions in stable contexts, the Lebanese case shows how involuntary contraction produces adaptive financial strategies that prioritize survival and resilience. This brings new insight into how degrowth dynamics play out in real-world crisis settings.

In addition, the framework bridges sustainable finance with political economy approaches to fragility. Research on fragile states has long centered on governance, aid, and macroeconomic instability, but rarely examines how financial practices evolve at the household or community level when formal institutions fail. By highlighting informal and resilience-driven mechanisms, this framework provides a foundation for analyzing financial systems “from below,” offering a more grounded understanding of finance in crisis contexts.

Policy Implications

The insights from this framework suggest that established approaches for expanding sustainable finance are poorly suited to fragile economies. Policies designed around green bonds, ESG reporting, or sustainability-linked loans presume institutional stability, strong regulatory oversight, and functioning markets, conditions that are absent in collapsed systems. Yet studies show that these instruments are particularly sensitive to uncertainty and regulatory instability (Arouri et al., 2025), highlighting why they are poorly suited to crisis-affected economies. Rather than attempting to replicate these tools, policy actors operating in fragile settings should focus on enabling the financial mechanisms that already sustain livelihoods and basic provisioning.

Concretely, this includes safeguarding remittance corridors through reduced transaction costs, regulatory facilitation, and access to reliable payment infrastructure; supporting community-based energy and infrastructure financing through small grants, guarantees, or pooled risk-sharing instruments; and adopting light-touch or hybrid regulatory approaches that recognize and stabilize informal financial systems instead of seeking premature formalization. Diaspora-finance mechanisms, mutual aid networks, and locally embedded savings and credit arrangements can thus be treated as legitimate components of sustainability policy rather than residual or temporary responses to crisis.

In this perspective, the role of policy shifts from enforcing formal compliance to enabling adaptive capacity, local agency, and continuity of essential social and ecological functions under conditions of institutional fragility.

Implications for Financial Practice

For practitioners, the framework underscores the need to rethink how sustainable finance is structured and delivered in fragile environments. Traditional metrics of risk, return, and impact are inappropriate when the primary financial objective is survival and social continuity rather than profit maximization. Financial institutions must adopt an agility-oriented approach, supporting small-scale, rapidly deployable, and context-sensitive projects that align with community resilience strategies.

This perspective calls for more flexible investment models, simplified reporting requirements, and new risk assessments that recognize the value of informal economic practices. By embracing local agency and adaptive behaviors, practitioners can design financial interventions that genuinely contribute to sustainability in crisis-prone settings.

Limitations and Future Research Directions

This study is conceptual in nature, and several limitations should be acknowledged. First, the proposed framework for Agile Sustainable Finance has not yet been empirically tested. While it is grounded in established literatures and illustrative evidence, future research is required to validate the proposed mechanisms and propositions through empirical investigation across different fragile and crisis-affected contexts.

Second, although the framework distinguishes between resilience and sustainability, some conceptual ambiguity between “resilience finance” and “sustainable finance” may remain. Further theoretical work is needed to clarify how short-term resilience practices translate into longer-term sustainability outcomes, particularly in environments characterized by prolonged instability.

Third, the framework is developed using Lebanon as an illustrative conceptual lens. While Lebanon provides a rich example of institutional collapse and adaptive financial behavior, the framework may not be directly generalizable to all fragile states, which differ widely in their political, social, and economic conditions. Comparative studies across multiple fragile and post-collapse economies would help assess the broader applicability of the proposed framework.

Finally, significant measurement challenges remain. Concepts such as agility, sustainability outcomes, and ecological sufficiency in informal financial systems are difficult to operationalize using conventional financial indicators. Future research could develop context-sensitive metrics and mixed-method approaches, including financial diaries, network analysis, and micro-level case studies, to better capture adaptive financial practices and their social and ecological implications.

Conclusion

This paper has argued that sustainable finance must be fundamentally reimagined in the context of fragile and crisis-affected economies. Conventional models assume institutional stability, functioning financial markets, and growth-oriented policy environments, conditions that are absent in places such as Lebanon. By integrating insights from sustainable finance, degrowth and post-growth theory, and the political economy of fragility, the paper has introduced Agile Sustainable Finance as a conceptual framework capable of explaining how financial life continues when formal mechanisms fail.

The framework demonstrates that sustainability does not disappear in the absence of institutions; rather, it takes new forms grounded in adaptability, community cooperation, and informal financial practices. In fragile economies, sustainability becomes a matter of resilience rather than growth, and agility emerges as the central capability through which individuals and communities navigate uncertainty. These dynamics highlight the limits of conventional sustainable-finance instruments and point to the need for models that reflect lived realities instead of institutional ideals.

By positioning agility at the core of sustainable finance in fragile contexts, this paper contributes to a more inclusive and context-sensitive understanding of financial behavior. It also opens new avenues for research and policy, urging scholars and practitioners to recognize the value of informal systems and the adaptive strategies that sustain communities in periods of collapse. Rethinking sustainable finance through the lens of fragility is not only analytically necessary but also practically urgent, as an increasing number of economies face prolonged instability and weakening institutional capacity. Agile Sustainable Finance offers a foundation for developing financial approaches that are responsive to these challenges and capable of supporting resilience, equity, and ecological balance in the most vulnerable settings.

In summary, this study shows that sustainable finance in fragile economies must be grounded in agility, resilience, and local agency rather than in formal institutional structures or growth-oriented assumptions. From a policy perspective, this implies shifting attention away from instruments that presuppose institutional stability, such as green bonds or ESG-based disclosure, toward enabling conditions that support adaptive financial practices, including remittance facilitation, community-based energy financing, light-touch engagement with informal financial systems, and diaspora-linked risk-sharing mechanisms.

At the same time, this work is subject to important limitations. The proposed framework is conceptual and has not yet been empirically tested; the distinction between resilience-oriented finance and sustainability-oriented finance may remain context-dependent; and the measurement of agility, sustainability outcomes, and ecological sufficiency in informal systems poses significant empirical challenges. These limitations point directly to future research opportunities, including comparative studies across fragile economies, micro-level analyses of informal financial practices, and empirical testing of the propositions advanced in this paper.

Funding Statement

No external funding was received.

Conflict of Interest

The author declare that there is no conflict of interest regarding the publication of this paper.

CRediT Authorship Contribution Statement

Nadia Khalife: The sole author was responsible for all aspects of the work, including conceptualization, methodology, analysis, and manuscript preparation.

Supplementary Materials

Supplementary material for this article is available online via https://doi.org/10.51300/JSE-2026-166.

Publisher Disclaimer

The statements, interpretations, and conclusions expressed in this article are solely those of the author(s) and do not necessarily reflect the views of their affiliated institutions, the publisher, the editors, or the reviewers. The publisher and the editorial team make no representations or warranties of any kind, express or implied, regarding the accuracy, completeness, or reliability of the content and shall not be held responsible for any errors or omissions or for any consequences arising from the use of the information contained in this publication. The publisher remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

References

- . Planned Economic Contraction: The Emerging Case for Degrowth. Environmental Politics, 21(3), 349--368. https://doi.org/10.2139/ssrn.1941089. CrossRef | Google Scholar

- . Role of Mobile Applications in Mitigating Challenges Faced by Informal Saving Groups. In Proceedings of the 2020 IST-Africa Conference (IST-Africa). IST-Africa Institute.

- . Does climate policy uncertainty shape the response of stock markets to oil price changes? Evidence from GCC stock markets. Journal of Environmental Management, 375, 124229--124229. https://doi.org/10.1016/j.jenvman.2025.124229. CrossRef | Google Scholar

- . Dynamic Connectedness and Hedging Effectiveness Between Green Bonds, ESG Indices, and Traditional Assets. European Financial Management, 31(5), 1704--1719. https://doi.org/10.1111/eufm.12561. CrossRef | Google Scholar

- . Principles and Frameworks for Sustainable Finance. Financial Innovation for Global Sustainability, 103--139. https://doi.org/10.1002/9781394311682.ch5. CrossRef | Google Scholar

- . When a financially oriented performance measurement system supports hybrid collective sensemaking: The case of a cooperative bank. The British Accounting Review, 56(5), 101202--101202. https://doi.org/10.1016/j.bar.2023.101202. CrossRef | Google Scholar

- . Walking a Tightrope: Using Financial Diaries to Investigate Day-to-Day Financial Decisions and the Social Safety Net of the Financially Excluded. The ANNALS of the American Academy of Political and Social Science, 689(1), 46--64. https://doi.org/10.1177/0002716220921154. CrossRef | Google Scholar

- . ESG performance, institutional factors, and the cost of debt. Journal of Sustainable Finance and Investment, 15(3), 523--551. https://doi.org/10.1080/20430795.2025.2489386. CrossRef | Google Scholar

- . ‘Informal’ Financial Practices in the South Bronx: Family, Compadres, and Acquaintances. Journal of Family and Economic Issues, 45(2), 327--342. https://doi.org/10.1007/s10834-023-09912-0. CrossRef | Google Scholar

- . Interactive effects of brand reputation and ESG on green bond issues: A sustainable development perspective. Business Strategy and the Environment, 32(1), 570--586. https://doi.org/10.1002/bse.3161. CrossRef | Google Scholar

- . Planning Beyond Growth the Case for Economic Democracy within Ecological Limits. Journal of Cleaner Production, . Elsevier BV, 437, 140351--140351. https://doi.org/10.2139/ssrn.4457481. CrossRef | Google Scholar

- . Exports, Exchange Regimes, and Fragility. Oxford University Press. https://doi.org/10.1093/oso/9780198853091.003.0014. CrossRef | Google Scholar

- . Analysis of the primary responsibilities of team leaders in extreme Iraqi Context. Management international, 28(5), 122--133. https://doi.org/10.59876/a-d4g0-52nf. CrossRef | Google Scholar

- . Imperfect financial markets and the cyclicality of social spending. European Economic Review, 167, 104786--104786. https://doi.org/10.1016/j.euroecorev.2024.104786. CrossRef | Google Scholar

- . Nudges for responsible finance? A survey of interventions targeted at financial decision making. Corporate Social Responsibility and Environmental Management, 31(2), 1203--1219. https://doi.org/10.1002/csr.2625. CrossRef | Google Scholar

- . The Role of Remittances in Shaping Income Inequality in Lebanon Before and After the Crisis: An Empirical Analysis Using Macroeconomic and Financial Perspectives. Sustainability, 17(14), 6464--6464. https://doi.org/10.3390/su17146464. CrossRef | Google Scholar

- . Resilient agility in volatile economies: institutional and organizational antecedents. Journal of Organizational Change Management, 33(1), 100--113. https://doi.org/10.1108/jocm-02-2019-0033. CrossRef | Google Scholar

- . When does CSR motivate investors? A simulation study. Recherches en Sciences de Gestion, N° 129(6), 93--124. https://doi.org/10.3917/resg.129.0093. CrossRef | Google Scholar

- . State Collusion or Erosion During a Sovereign Debt Crisis: Market Dynamics Spawn Informal Practices in Lebanon. Springer International Publishing. https://doi.org/10.1007/978-3-030-82499-0_11. CrossRef | Google Scholar

- . Performance, economic, and environmental assessment of PV and PVT systems in Lebanon: A comparative case study. Energy Conversion and Management: X, 28, 101270--101270. https://doi.org/10.1016/j.ecmx.2025.101270. CrossRef | Google Scholar

- . What does degrowth mean? A few points of clarification. Globalizations, 18, 1105--1111. https://doi.org/10.1080/14747731.2020.1812222. CrossRef | Google Scholar

- . Fit for purpose? Clarifying the critical role of profit for sustainability. Journal of Political Ecology, 27(1), 236--262. https://doi.org/10.2458/v27i1.23502. CrossRef | Google Scholar

- . Prosperity without growth: Economics for a finite planet. Prosperity without growth: Economics for a finite planet. Earthscan.

- . Post-growth: the science of wellbeing within planetary boundaries. The Lancet Planetary Health, 9(1), 62--e78. https://doi.org/10.1016/s2542-5196(24)00310-3. CrossRef | Google Scholar

- . Sustainability of community-owned mini-grids: evidence from India. Energy, Sustainability and Society, 9(1). https://doi.org/10.1186/s13705-018-0185-9. CrossRef | Google Scholar

- . ESG lending. Journal of Financial Economics, 173, 104150--104150. https://doi.org/10.1016/j.jfineco.2025.104150. CrossRef | Google Scholar

- . Rethinking the Role of Informality as a Barrier to Financial Inclusion: Insights from an Indian Urban Setting. South Asia: Journal of South Asian Studies, 48(4), 824--845. https://doi.org/10.1080/00856401.2025.2538338. CrossRef | Google Scholar

- . A Framework for Conceptual Contributions in Marketing. Journal of Marketing, 75(4), 136--154. https://doi.org/10.1509/jmkg.75.4.136. CrossRef | Google Scholar

- . Institutional Breakdown? An Exploratory Taxonomy of Australian University Failure 1. Prometheus, 23(4). https://doi.org/10.1080/08109020500350237. CrossRef | Google Scholar

- . Green Finance and the Energy Transition: A Systematic Review of Economic Instruments for Renewable Energy Deployment in Emerging Economies. Energies, 18, 4560--4560. https://doi.org/10.3390/en18174560. CrossRef | Google Scholar

- . Overcoming Agricultural Challenges with GMOs as a Catalyst for Poverty Reduction and Sustainability in Lebanon. Sustainability, 15(23), 16187--16187. https://doi.org/10.3390/su152316187. CrossRef | Google Scholar

- . Lebanese Banking System: Ponzi or Not?. Journal of Law and Sustainable Development, 11(6), 11--11. https://doi.org/10.55908/sdgs.v11i6.1204. CrossRef | Google Scholar

- . The future is degrowth: A guide to a world beyond capitalism. Verso Books.

- . How does institutional quality respond to banking crises occurrences?. International Review of Economics, 72(2). https://doi.org/10.1007/s12232-025-00496-9. CrossRef | Google Scholar

- . Financing in fragile contexts. .

- . An environmental assessment through load capacity factor: the dynamic effects of technological cooperation grants and energy depletion in Pakistan. Frontiers in Sustainable Energy Policy, 3, 1438573--1438573. https://doi.org/10.3389/fsuep.2024.1438573. CrossRef | Google Scholar

- . Clean energy initiatives in Pakistan: Driving sustainable development and lowering carbon emissions through environmental innovation and policy optimization. Journal of Environmental Management, 373, 123647--123647. https://doi.org/10.1016/j.jenvman.2024.123647. CrossRef | Google Scholar

- . Unpacking the role of green supply chain and renewable energy innovation in advancing environmental sustainability: A Quantile-Based approach. Renewable and Sustainable Energy Reviews, 218, 115810--115810. https://doi.org/10.1016/j.rser.2025.115810. CrossRef | Google Scholar

- . Unveiling the green path: The role of green finance and just energy transition in environmental sustainability. Gondwana Research, 148, 348--367. https://doi.org/10.1016/j.gr.2025.07.024. CrossRef | Google Scholar

- . Remittances in Fragile and Conflict-Affected Settings: Insights from Myanmar. The European Journal of Development Research, 37(6), 1013--1043. https://doi.org/10.1057/s41287-025-00712-w. CrossRef | Google Scholar

- . Rotating savings and credit associations: A scoping review. World Development Sustainability, 3, 100081--100081. https://doi.org/10.1016/j.wds.2023.100081. CrossRef | Google Scholar

- . Institutional fragility at the boundary: reframing systemic decline as a crisis of recalibration. Theory and Society, 54(6), 1103--1118. https://doi.org/10.1007/s11186-025-09657-9. CrossRef | Google Scholar

About contributors

Nadia Khalife

Faculty of Business Administration and Economics, Notre Dame University - Louaize, Zouk Mosbeh, Lebanon

Lebanon